Page 158 - Hitachi IR 2025

P. 158

MANAGEMENT DISCUSSION & ANALYSIS

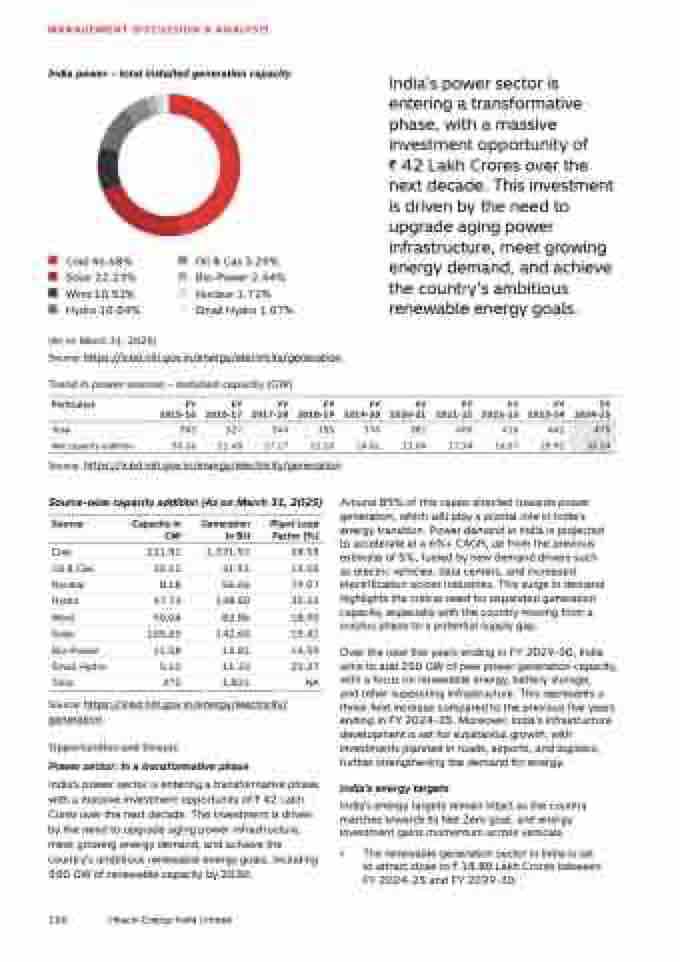

India power – total installed generation capacity

Coal 46.68% Oil & Gas 5.29%

Solar 22.23% Bio-Power 2.44%

Wind 10.53% Nuclear 1.72%

Hydro 10.04% Small Hydro 1.07%

India's power sector is

entering a transformative

phase, with a massive

investment opportunity of

` 42 Lakh Crores over the

next decade. This investment

is driven by the need to

upgrade aging power

infrastructure, meet growing

energy demand, and achieve

the country’s ambitious

renewable energy goals.

(As on March 31, 2025)

Source: https://iced.niti.gov.in/energy/electricity/generation

Trend in power sources – installed capacity (GW)

Particulars FY

2015-16

FY

2016-17

FY

2017-18

FY

2018-19

FY

2019-20

FY

2020-21

FY

2021-22

FY

2022-23

FY

2023-24

FY

2024-25

Total 305 327 344 356 370 382 400 416 442 475

Net capacity addition 30.26 21.68 17.17 12.10 14.01 12.04 17.34 16.57 25.92 33.24

Source: https://iced.niti.gov.in/energy/electricity/generation

Source-wise capacity addition (As on March 31, 2025)

Source Capacity in

GW

Generation

in BU

Plant Load

Factor (%)

Coal 221.81 1,331.92 68.55

Oil & Gas 25.12 31.91 14.50

Nuclear 8.18 56.66 79.07

Hydro 47.73 148.50 35.52

Wind 50.04 82.86 18.90

Solar 105.65 142.60 15.41

Bio-Power 11.58 14.81 14.59

Small Hydro 5.10 11.33 25.37

Total 475 1,821 NA

Source: https://iced.niti.gov.in/energy/electricity/

generation

Opportunities and threats

Power sector: In a transformative phase

India's power sector is entering a transformative phase,

with a massive investment opportunity of ` 42 Lakh

Cores over the next decade. This investment is driven

by the need to upgrade aging power infrastructure,

meet growing energy demand, and achieve the

country’s ambitious renewable energy goals, including

500 GW of renewable capacity by 2030.

Around 85% of this capex directed towards power

generation, which will play a pivotal role in India's

energy transition. Power demand in India is projected

to accelerate at a 6%+ CAGR, up from the previous

estimate of 5%, fueled by new demand drivers such

as electric vehicles, data centers, and increased

electrification across industries. This surge in demand

highlights the critical need for expanded generation

capacity, especially with the country moving from a

surplus phase to a potential supply gap.

Over the next five years ending in FY 2029-30, India

aims to add 250 GW of new power generation capacity,

with a focus on renewable energy, battery storage,

and other supporting infrastructure. This represents a

three-fold increase compared to the previous five years

ending in FY 2024-25. Moreover, India’s infrastructure

development is set for substantial growth, with

investments planned in roads, airports, and logistics,

further strengthening the demand for energy.

India’s energy targets

India’s energy targets remain intact as the country

marches towards its Net Zero goal, and energy

investment gains momentum across verticals.

• The renewable generation sector in India is set

to attract close to ` 18.80 Lakh Crores between

FY 2024-25 and FY 2029-30.

156 Hitachi Energy India Limited